For businesses currently importing from, and exporting to, non-EU Countries, the world of customs duty and commodity codes will be familiar territory.

From 1 January 2021 when the transitional period ends, Brexit will take full effect - goods arriving into the UK from the EU will be imports and goods sent from the UK to the EU will be exports in VAT terms. From that point, the commodity code and import duty rules will be vital for UK businesses who previously relied mainly on the EU for sales and purchases.

A commodity code consists of ten digits - the first six are based on the 'harmonised system' which define the product and are split between chapter, heading, and sub-heading.

The next two digits relate to the 'combined nomenclature' which further define the product and are dependent upon the product. The final two digits relate to additional scenarios and there can be a further two added as well, giving a total of twelve.

As well as determining the import duty payable, the commodity codes can also identify if a product requires a license, permit or other such document before importation or exportation can take place. For example, we know that from April 2021, health certificates and pre-notification will be required for products of animal origin and plants.

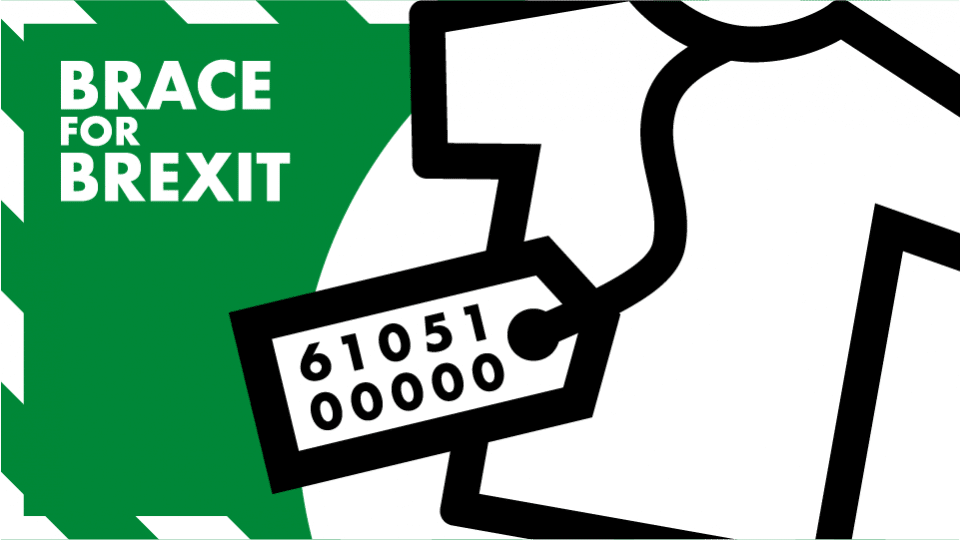

If importing blouses for women, it is 61062000000, the code is (61) again denoting articles of clothing, 06 (womens’ and girls’ blouses), 20 (this time synthetic fibres, not cotton). Both shirts and blouses have an import duty rate of 12%.

Before 1 January 2021 the 12% duty would be added only for goods entering from outside of EU, but from that date, that code will apply to all goods arriving into the UK from anywhere in the world. For a UK retailer who specialises in fine Italian clothing, who only sources goods from Italy, that potentially adds 12% to the sellers selling price.

Import duty is not recoverable and therefore becomes a cost to the business.

Post Brexit, the UK has introduced a 'UK Global Tariff' which may be subject to change if there is a deal with the EU.

If there is no deal then the UK Global tariffs come into effect 1 January 2021, so there is a little uncertainty here but no reason not to start reviewing your commodity codes now. It makes good sense to consider the risks and threats to your business.

Assuming the UK Global Tariff is the defacto duty rates, here is another example:

The EU currently has an import duty rate of 3.2% for guitars entering the EU from a non-EU source. If the shop buys a guitar from Spain for £1,000 then importing it into the UK will add £32 in import duty. Pre-Brexit this would have been duty free. Post Brexit, the UK duty rate is 2% so an import duty of £20.

This works in reverse as well, so a UK retailer selling a guitar to a Spanish customer will see the UK sale zero rated for VAT. On arrival into Spain, Spanish customs will assess duty of 3.2% plus Spanish VAT and will not release the goods until the customer or shipping agent pays this duty and VAT. Thus there is potential additional costs selling to EU and buying from the EU.

A future article will consider the customer’s experience and who the importer of the goods will be, the seller or the customer, and the impact this has on these parties.

From 1 January 2021 when the transitional period ends, Brexit will take full effect - goods arriving into the UK from the EU will be imports and goods sent from the UK to the EU will be exports in VAT terms. From that point, the commodity code and import duty rules will be vital for UK businesses who previously relied mainly on the EU for sales and purchases.

What is a commodity code?

Commodity codes define the goods, and they determine the import duty payable on those goods. Therefore, ensuring that the right commodity code is applied is key to gaining compliance and ensuring your profit margins are correctly calculated.A commodity code consists of ten digits - the first six are based on the 'harmonised system' which define the product and are split between chapter, heading, and sub-heading.

The next two digits relate to the 'combined nomenclature' which further define the product and are dependent upon the product. The final two digits relate to additional scenarios and there can be a further two added as well, giving a total of twelve.

As well as determining the import duty payable, the commodity codes can also identify if a product requires a license, permit or other such document before importation or exportation can take place. For example, we know that from April 2021, health certificates and pre-notification will be required for products of animal origin and plants.

Example 1

You intend to import some fine shirts for men from Italy, and the commodity code is 6105100000 broken down as 61 (Articles of clothing/apparel), 05 (mens’ or boys’ shirts), 10 (cotton).If importing blouses for women, it is 61062000000, the code is (61) again denoting articles of clothing, 06 (womens’ and girls’ blouses), 20 (this time synthetic fibres, not cotton). Both shirts and blouses have an import duty rate of 12%.

Before 1 January 2021 the 12% duty would be added only for goods entering from outside of EU, but from that date, that code will apply to all goods arriving into the UK from anywhere in the world. For a UK retailer who specialises in fine Italian clothing, who only sources goods from Italy, that potentially adds 12% to the sellers selling price.

Import duty is not recoverable and therefore becomes a cost to the business.

Post Brexit, the UK has introduced a 'UK Global Tariff' which may be subject to change if there is a deal with the EU.

If there is no deal then the UK Global tariffs come into effect 1 January 2021, so there is a little uncertainty here but no reason not to start reviewing your commodity codes now. It makes good sense to consider the risks and threats to your business.

Assuming the UK Global Tariff is the defacto duty rates, here is another example:

Example 2

A shop imports guitars for sale in the UK. The commodity code is 92 (musical instruments), 02 (other stringed instruments), 90 (other than instruments played with a bow), 30 (guitars) = 9202903000.The EU currently has an import duty rate of 3.2% for guitars entering the EU from a non-EU source. If the shop buys a guitar from Spain for £1,000 then importing it into the UK will add £32 in import duty. Pre-Brexit this would have been duty free. Post Brexit, the UK duty rate is 2% so an import duty of £20.

This works in reverse as well, so a UK retailer selling a guitar to a Spanish customer will see the UK sale zero rated for VAT. On arrival into Spain, Spanish customs will assess duty of 3.2% plus Spanish VAT and will not release the goods until the customer or shipping agent pays this duty and VAT. Thus there is potential additional costs selling to EU and buying from the EU.

What is needed

A business may require knowledge of both the UK duty rates (if importing from EU) and also the EU duty rates (if exporting to EU). The commodity codes will not change but the duty rates associated with those codes may.A future article will consider the customer’s experience and who the importer of the goods will be, the seller or the customer, and the impact this has on these parties.